What the Refinance Calculator Does

Enter your current loan (balance, rate, remaining term) and the new offer (rate, term, closing costs), and the calculator returns:

- Monthly savings — the drop in your P&I payment after refinancing

- Break-even month — when cumulative savings first exceed closing costs

- Net savings at multiple horizons — 5, 10, 15, and 30 years

- Cumulative savings chart — how savings build over time, starting below zero at closing

It handles rate-and-term refinances (same balance, new rate/term) and cash-out refinances (larger new loan; extract equity as cash).

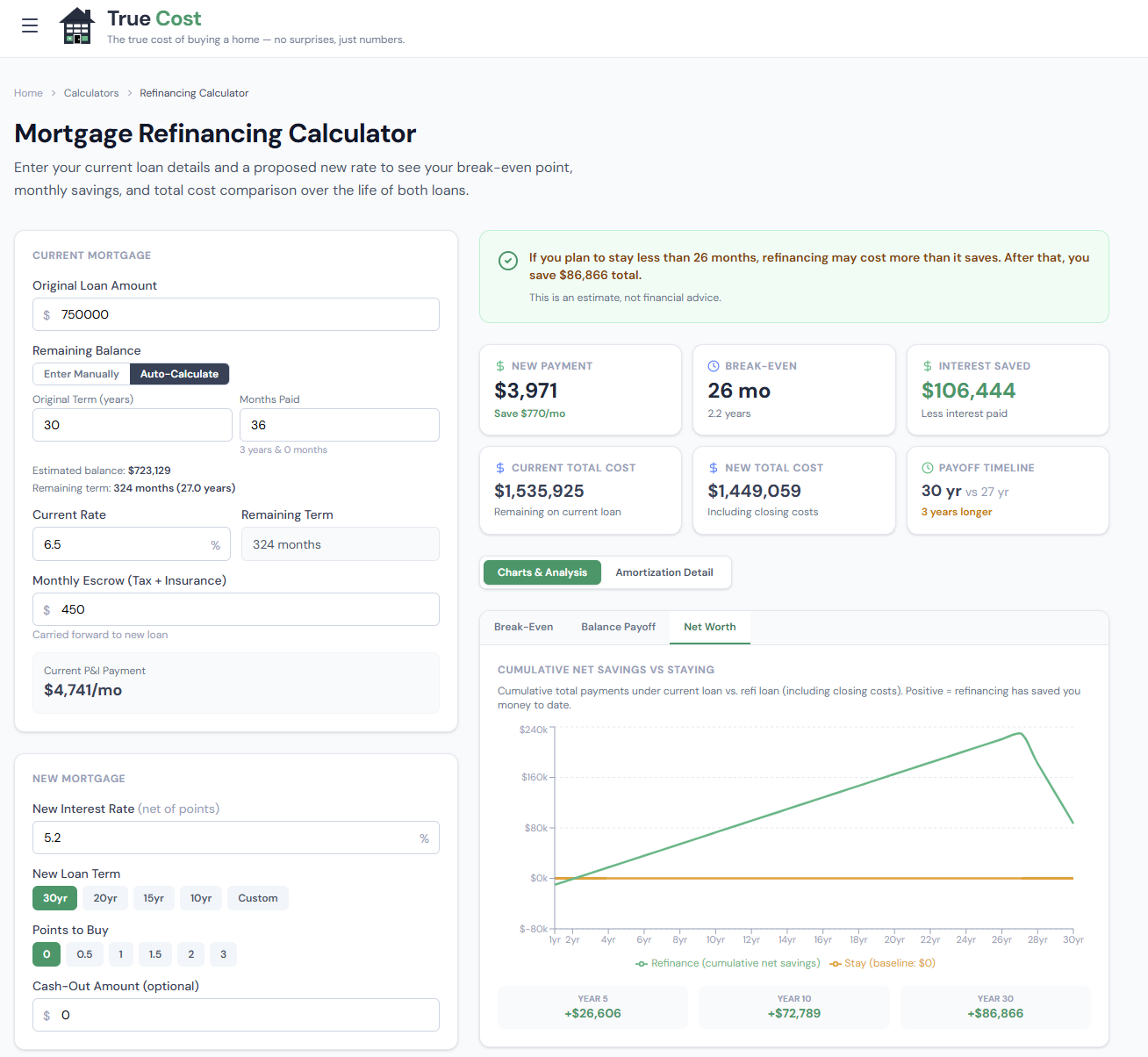

The Inputs Panel

The inputs are divided into two sections: your current loan and the new loan offer. Getting these right is the key to an accurate analysis.

click to enlarge

click to enlarge

Current Loan Inputs

| Input | Where to find it |

|---|---|

| Current Rate | Your mortgage statement or original loan documents |

| Remaining Balance | Your most recent mortgage statement |

| Remaining Term | Original term minus months paid (e.g., 30yr − 5yr = 300 months remaining) |

| Current Monthly P&I | Your mortgage statement (principal + interest only, not escrow) |

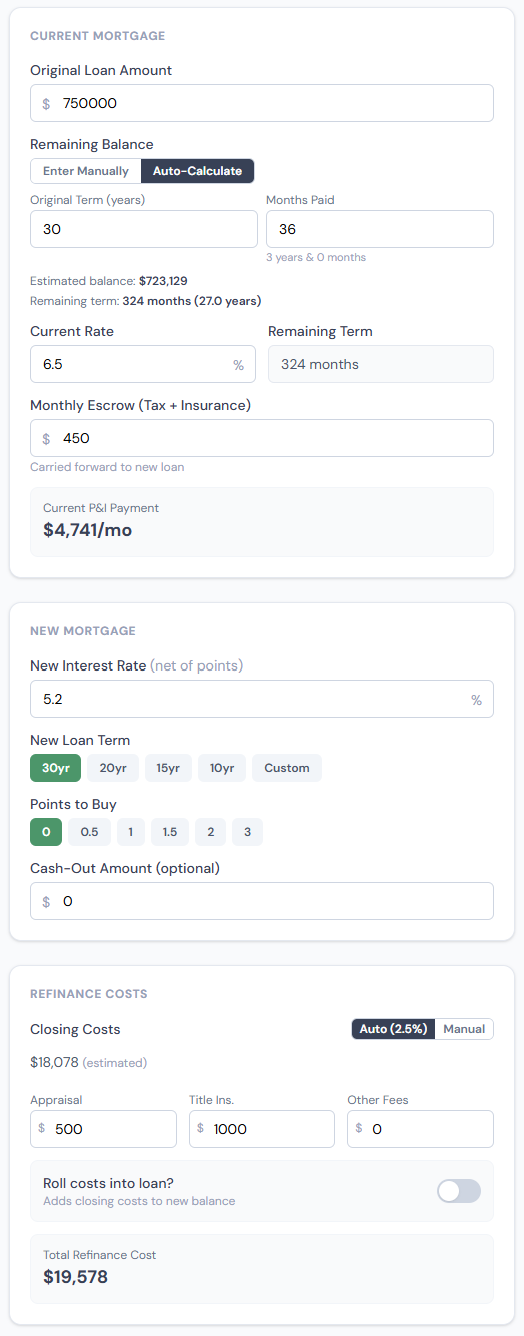

New Loan Inputs

| Input | Notes |

|---|---|

| New Rate | Get this from a Loan Estimate from your lender |

| New Term | Typically 30 or 15 years; resetting to 30 extends your payoff date |

| Cash Out Amount | 0 for a rate-and-term refi; enter the lump sum if pulling equity |

| Closing Costs | Typically 2–3% of loan amount; get from your lender's Loan Estimate |

| Roll Closing Costs | Whether to add costs to the loan (no upfront cash) or pay at closing |

Where the Break-Even Gets Tricky: Term Resets

This is the input most people get wrong. If you have 22 years left on your current mortgage and you refinance into a new 30-year loan, you've just added 8 years of payments. Your monthly payment drops, but your total interest may actually be higher than staying the course — because you're now amortizing over a much longer period.

The calculator models this correctly. It compares cumulative interest on your current loan (remaining 22 years) vs. the new loan (30 years) — not just monthly payments. If the break-even looks great but the 10-year net savings are surprisingly small, a term extension is probably why.

How the Break-Even Is Calculated

Monthly P&I savings = Current P&I − New P&I

Simple break-even = Closing costs ÷ Monthly savings

For example: $6,000 closing costs ÷ $350/month savings = 17.1 months. At month 18, you've recovered the cost of refinancing.

The calculator also shows an adjusted break-even that accounts for the opportunity cost of the closing costs — what you'd earn if that $6,000 were invested instead. This slightly extends the true break-even but is more financially precise.

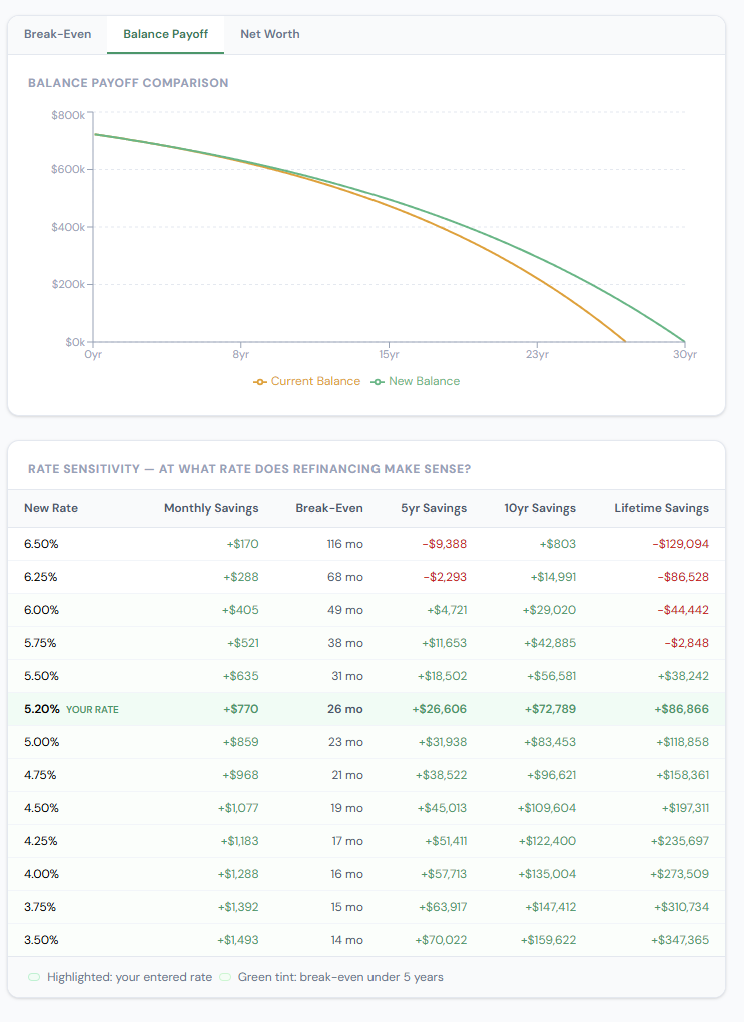

Reading the Cumulative Savings Chart

The chart is where the full picture becomes clear.

click to enlarge

click to enlarge

The savings line starts below zero — that's the closing cost you paid upfront. Each month after that, your P&I savings push the line up. When the line crosses zero, you've broken even. From there, every month is net positive.

What to look for on the chart:

- Slope of the line: A steep upward slope means large monthly savings and a fast payoff. A shallow slope means modest savings and a long break-even.

- Shape change around year 3–5: If you have a term extension, the chart may appear favorable early but flatten or turn negative later as the extended interest accrual catches up.

- Your expected horizon: Draw an imaginary vertical line at the year you expect to sell or refinance again. Is the savings line above zero by then? By how much?

Net Savings at Multiple Time Horizons

The table below the chart shows net savings at 5, 10, 15, and 30 years. This is total interest saved minus closing costs — the actual financial outcome at each horizon.

Use your expected ownership horizon as the reference point. If you're planning to stay 7 years:

- Look at year 5 (conservative): is the number meaningfully positive?

- Look at year 10 (optimistic): confirms the trajectory

If net savings at year 7 are $4,000 on $6,000 of closing costs, the math barely pencils out. If it's $18,000, it's a clear win.

Rate-and-Term vs. Cash-Out Refinance

Rate-and-term refinance — you're replacing your current loan with a new one at a lower rate or shorter term. The new loan amount equals your remaining balance. Monthly payment drops; closing costs are the only upfront cost. This is the cleanest scenario to analyze and the most common reason to refinance.

Cash-out refinance — the new loan amount is your remaining balance plus the cash you're extracting. Your new monthly payment may be higher than your current one (larger loan), but you receive a lump sum at closing. The calculator shows when the lump sum benefit is offset by the higher interest cost going forward.

Cash-out refinances make most sense when:

- Your current rate is higher than available rates (you'd benefit from a rate drop anyway)

- You're using the cash for a high-ROI purpose: home renovation, debt consolidation at higher rates, or investment

- Your remaining balance is large enough that the cash-out doesn't meaningfully raise your loan-to-value ratio

When Refinancing Makes Sense

Strong case for refinancing:

- Break-even month is well within your expected remaining ownership horizon (ideally less than half)

- Rate drop is 0.75%+ (smaller drops rarely cover closing costs in reasonable time)

- You're not planning to move or refinance again within 2–3 years

- You have stable employment and can qualify for the new loan

- Closing costs are reasonable (some lenders quote 4%+ — shop around)

Wait or skip:

- You're within 5–7 years of payoff — resetting to a longer term rarely makes sense even at a lower rate

- The break-even is longer than your expected remaining ownership

- Rates are falling and you expect another drop — refinancing twice in 12 months doubles costs

- Your loan balance is very small — the closing cost payback period extends dramatically

Rolling Closing Costs Into the Loan

When you roll closing costs into the loan (common for borrowers who are cash-constrained), you don't pay upfront — but you're borrowing slightly more and paying interest on the closing costs for the life of the loan. The monthly payment is also slightly higher than it would be if you paid costs at closing.

The calculator handles this correctly: the balance used for the new loan is remaining balance + closing costs, and the P&I is recalculated from that higher starting point. Your break-even is faster (no upfront cash out), but your cumulative savings over time are slightly reduced.

Frequently Asked Questions

What's a typical break-even month for a refinance? Most refinances break even in 18–36 months. Break-evens under 12 months are unusual (very large savings, very low closing costs) but represent a slam dunk. Over 48 months, you need high confidence in your long-term housing plans.

How do I get an accurate closing cost estimate? Apply for the refinance and request a Loan Estimate (LE) from the lender — they're required to provide one within 3 business days. The LE itemizes every fee. Common components: origination fee (0–1% of loan), appraisal ($400–$600), title insurance ($800–$1,500), prepaid interest, recording fees. A cash-out refi on a larger loan will have higher costs.

What's a "no-closing-cost" refinance? Some lenders offer no upfront costs by building the costs into a slightly higher rate. You pay nothing at closing, but your rate is 0.125–0.25% higher than it would be otherwise. This is advantageous if you plan to refinance or sell again within a few years — the higher rate costs less than the sunk closing costs would. The break-even calculation still applies; it's just that your "cost" is the permanently higher rate rather than an upfront cash outflow.

Should I refinance from a 30-year to a 15-year loan? A 15-year refinance dramatically reduces total interest but significantly raises monthly payments — often 30–40% more for the same balance. The break-even is usually fast (you're saving so much interest), but cash flow impact is large. Run both the 15-year and 30-year scenarios in the calculator and compare net savings at your horizon alongside the monthly payment impact.

My lender says I'll save $400/month — why does the calculator show a different number? Lenders often quote payment savings including escrow (taxes and insurance), which don't change with a refinance — only the P&I portion changes. The calculator works with P&I savings only, which is the accurate measure of refinance benefit. Escrow changes are a separate budget adjustment, not a refinance saving.