The Core Concept: Marginal Benefit

The key to understanding the mortgage interest deduction is understanding marginal benefit. The deduction doesn't save you money equal to your tax rate times your mortgage interest. It only saves you money on the amount by which your total itemized deductions exceed the standard deduction.

Example where the deduction has zero value:

- Standard deduction (married filing jointly, 2026): $30,000

- Your mortgage interest: $20,000

- Your property taxes (SALT cap at $10,000): $10,000

- Total itemized: $30,000

- Marginal benefit: $0 — you'd take the standard deduction anyway

Example where the deduction provides real value:

- Standard deduction: $30,000

- Your mortgage interest: $28,000

- Your property taxes (SALT cap): $10,000

- Total itemized: $38,000

- Amount above standard deduction: $8,000

- At 24% federal + 6% state: tax savings = $8,000 × 30% = $2,400/year

The Tax Benefit Calculator does this math precisely — and then repeats it for every year of your loan as interest payments shrink.

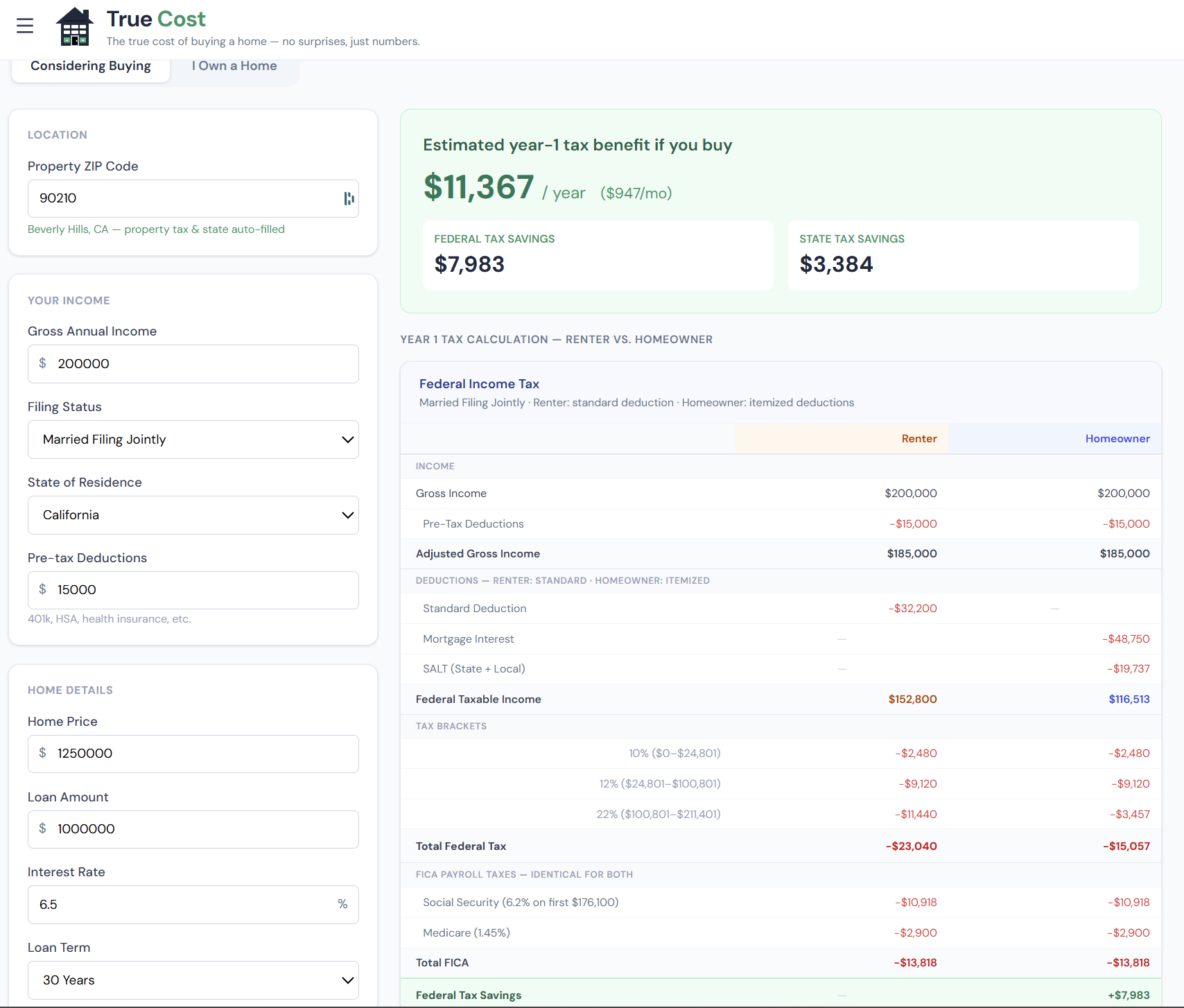

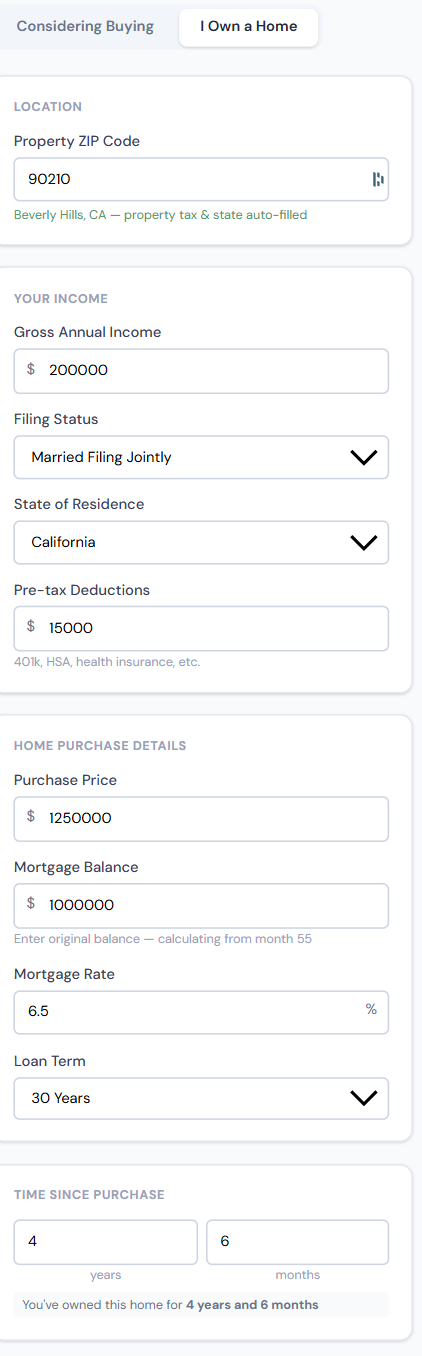

The Inputs Panel

The inputs panel collects everything needed to compute your specific marginal benefit.

click to enlarge

click to enlarge

| Input | Purpose |

|---|---|

| Loan Amount | Used to compute annual mortgage interest |

| Interest Rate | Your mortgage rate (not APR) |

| Gross Annual Income | Determines your federal and state tax bracket |

| Filing Status | Single, MFJ, or Head of Household — sets standard deduction |

| State of Residence | Pulls state income tax rate from the True Cost tax database |

| Pre-Tax Deductions | 401(k), HSA contributions — reduce AGI before bracket calc |

| Property Tax Rate | Auto-fills from ZIP; used for SALT calculation |

| Additional Deductions | Charitable donations, other itemizable expenses |

Why Pre-Tax Deductions Matter

Pre-tax deductions (401k contributions, HSA contributions, health insurance premiums) reduce your Adjusted Gross Income (AGI) — the income figure used to determine which bracket you're in. A household with $180,000 gross income and $24,000 in 401k contributions is taxed at 22% marginal rates rather than 24%. That one bracket difference changes the deduction's value by nearly 10%.

The SALT Cap and Property Taxes

SALT (State and Local Taxes) deductions are capped at $10,000 combined for property taxes and state income taxes. If your property tax alone is $14,000/year, you can only deduct $10,000 — limiting the itemized total and thus the marginal benefit. This cap hits hardest in high-property-tax states (New Jersey, Illinois, Connecticut) and high-income-tax states (California, New York).

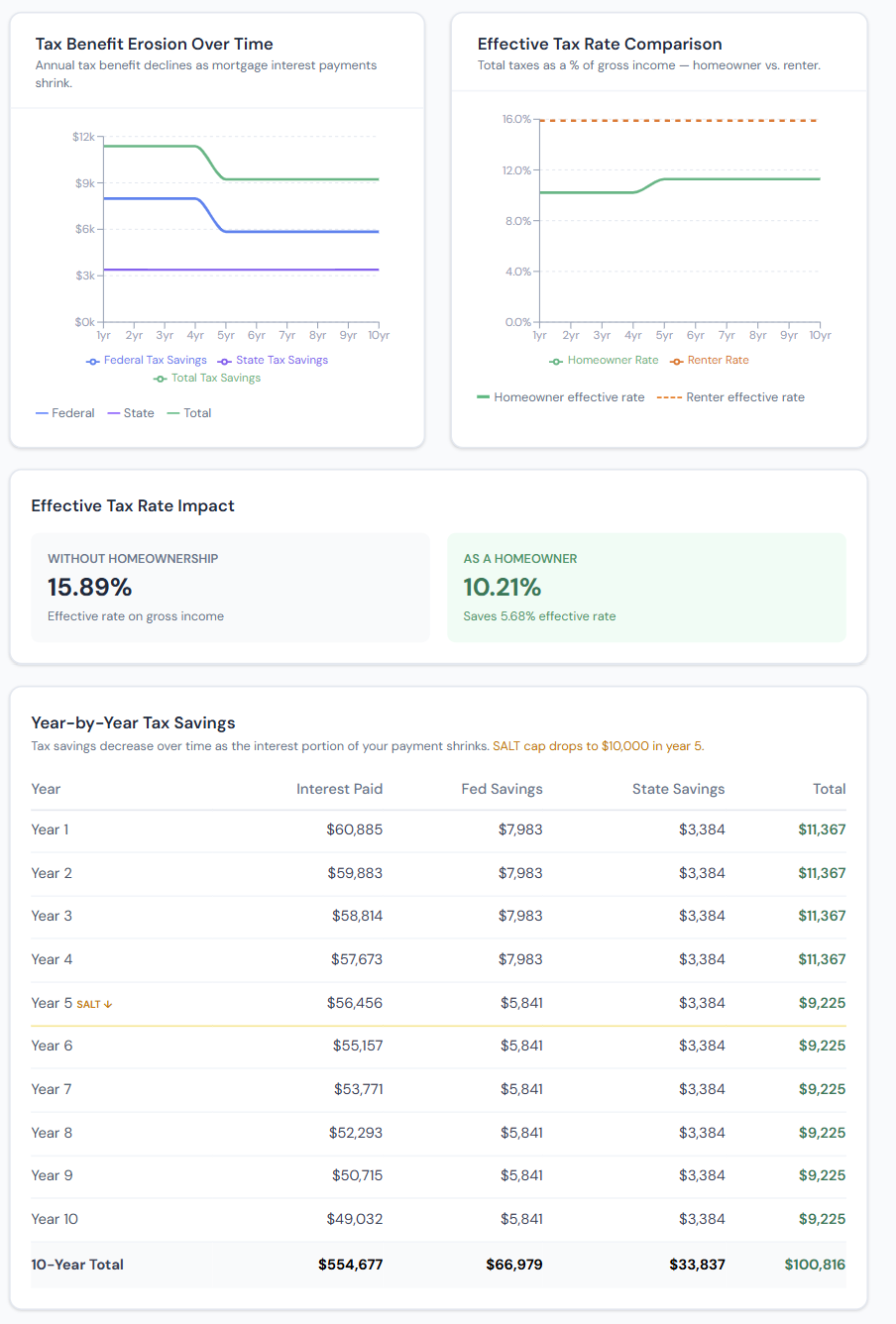

The Results: Year 1 and Beyond

The results panel shows both the immediate year-1 benefit and how it changes over time.

click to enlarge

click to enlarge

Year 1 Analysis

Annual tax savings — The dollar amount saved in year 1. For most borrowers in the 22–24% bracket with a $400,000+ loan above the standard deduction threshold, this is typically $1,000–$3,500. Borrowers at or below the threshold get $0.

Effective after-tax rate — What your mortgage effectively costs you per year after the deduction. If your rate is 7% and the deduction is worth $2,000/year on a $400,000 loan, your effective rate is roughly 6.5%. This is the number to compare to alternative uses of capital.

Itemized vs. standard deduction chart — Shows your total itemized deductions alongside the standard deduction threshold. The gap above the threshold is your marginal benefit zone. When the itemized line falls below the standard deduction line, the deduction is worthless.

The Erosion Over Time

This is what most mortgage tools don't show: the deduction value is highest in year 1 and falls every single year as your principal paydown reduces interest charges.

The erosion chart shows this decline explicitly. For a 7% loan on $400,000, the trajectory looks roughly like:

| Year | Annual Interest | Deduction Benefit | After-Tax Rate |

|---|---|---|---|

| 1 | ~$27,700 | $2,300 | ~6.43% |

| 5 | ~$26,400 | $2,100 | ~6.47% |

| 10 | ~$24,200 | $1,600 | ~6.60% |

| 15 | ~$21,400 | $700 | ~6.82% |

| 20 | ~$17,600 | $0 | 7.00% |

By year 20, interest has dropped enough that itemized deductions fall back below the standard deduction — and the effective rate equals the nominal rate.

The crossover year — When your itemized deductions drop to the standard deduction level — is one of the most important outputs. After this year, the deduction provides no benefit and the tax calculation is irrelevant to your housing decision.

What This Means for Your Decision

The tax benefit affects three calculations in the True Cost suite:

Buy vs. Rent break-even: The deduction makes buying cheaper than it appears in early years, shortening the break-even. But since the benefit erodes, the advantage is front-loaded — and most buy-vs-rent analyses overstate it by applying year-1 deduction rates to all 30 years.

Extra payment ROI: If your after-tax effective rate is 6.2%, that's the hurdle rate for extra payments vs. investing. An investment return above 6.2% (after tax) beats extra payments; below it, extra payments win.

Refinance decisions: When evaluating a refinance, the relevant rate to compare is the after-tax rate on both your current loan and the new offer. If refinancing drops your rate from 7% to 6%, but your effective after-tax rates are 6.2% vs. 5.6%, the real savings are smaller than the nominal rate difference suggests.

Common Misconceptions

"The deduction saves me my tax rate times my interest." Only true if you're well above the standard deduction threshold. If your total itemized deductions barely exceed the standard deduction, you're only getting a benefit on the small margin above it — not on all your interest.

"The deduction makes homeownership affordable." For most borrowers post-TCJA, the deduction provides modest benefit (if any). It's not a structural affordability tool — it's a modest government subsidy that phases out as your loan ages.

"I'll always be able to itemize because of my mortgage." Not if the standard deduction keeps rising (it's indexed to inflation). And not if your mortgage balance — and thus interest payments — shrinks enough over time. Many borrowers who itemized in year 1 are taking the standard deduction by year 12.

"The SALT cap doesn't affect me." The SALT cap limits your combined property tax + state income tax deduction to $10,000. In any state where those two costs exceed $10,000 combined — which includes many metros even in moderate-income-tax states — you're capped. That reduces your itemized total and thus the marginal benefit of the mortgage deduction.

Step-by-Step Walkthrough

- Enter your loan amount and interest rate

- Enter your gross annual income and filing status

- Select your state of residence — the calculator loads the correct marginal rates

- Enter your property tax rate (auto-fills from ZIP if set)

- Add any pre-tax deductions (annual 401k contributions, HSA max, etc.)

- Add additional itemized deductions if applicable (charitable giving, etc.)

- Review your annual tax savings and effective after-tax rate in year 1

- Check the crossover year — when the benefit goes to zero

- Review the deduction erosion chart — how quickly the benefit fades

Frequently Asked Questions

Why does my deduction seem smaller than what my lender told me? Lenders sometimes quote the gross deduction (interest × rate) without subtracting the standard deduction threshold. Only the amount above the standard deduction is your actual benefit. A $28,000 interest deduction with a $30,000 standard deduction means your actual benefit is $0.

My state has no income tax — does that change my analysis? Yes — in states with no income tax (Texas, Florida, Washington, Nevada, etc.), the SALT deduction only consists of property taxes. If your property taxes are under $10,000/year, you're not SALT-capped. But you also lose the state-level deduction benefit, since there's no state income tax to reduce. The federal benefit still applies if you're above the standard deduction threshold.

Does the $750,000 mortgage limit affect me? Loans originated after December 15, 2017 are subject to a deductibility limit: only interest on the first $750,000 of debt is deductible. If your loan is $900,000, only about 83% of your interest qualifies. The calculator applies this limit automatically when your loan exceeds $750,000.

How does this change if the TCJA standard deduction expires? The doubled standard deduction was set to expire after 2025 but was extended. If the standard deduction reverts to pre-TCJA levels (roughly half), many more homeowners would benefit meaningfully from itemizing. The calculator uses current 2026 law.

Is the mortgage interest deduction worth it for first-time buyers? Statistically, many first-time buyers in mid-price markets get limited benefit because their loans are smaller and their combined itemized deductions don't significantly exceed the standard deduction. The calculator will tell you exactly where you land. Don't assume you're getting a large deduction — verify it with your actual numbers.